Welcome to the November edition of Tax news. We hope that you find this informative. Please contact us if you wish to discuss any matters in more detail.

SALARY OR DIVIDEND BEST IN 2023/24?

In recent years many accountants have advised their director/shareholder clients that the most tax efficient method of extracting profit from their family company was to pay themselves a low salary, at or around the £12,570 personal allowance, with the balance in dividends.

This strategy may need to be revisited with the introduction of higher corporation tax rates from 1 April 2023 as company profits in excess of £50,000 are taxed at an effective 26.5% rate. Where company profits exceed £50,000 it may be more tax efficient to increase the salary or put a bonus through the company accounts.

There are lots of factors to take into account, including the level of profit and how much you need to draw out of the company to live on. We would suggest that we set up a meeting with you a couple of months before the company year end so that we can give you the best advice.

YEAR END TAX PLANNING IDEAS FOR YOUR BUSINESS

As mentioned above it is always a good idea to set up a planning meeting with us a couple of months before your business year end so that we can advise you on the best actions to take to reduce your taxable profits. In addition to considering paying yourself a bonus from your company you might consider:

- Bringing forward expenditure on equipment to take advantage of the 100% annual investment allowance (AIA) – up to £1 million a year on new and used equipment;

- For limited companies, most new equipment qualifies for unlimited “full expensing” relief;

- Where equipment is bought on hire purchase, make sure that it is brought into use by the year end to get tax relief on the full purchase price; and

- Making additional pension contributions, taking advantage of the new £60,000 annual input allowance.

CHARGING ELECTRIC CARS AT HOME

HMRC have recently clarified their view of the tax treatment of the reimbursement of electricity costs where employees charge their electric company cars at home. HMRC now accepts that reimbursing part of a domestic energy bill, which is used to charge a company car or van, is exempt from income tax. Their previous view was that such reimbursements were taxable.

Note that the exemption will only apply provided it can be demonstrated that the electricity was used to charge the company car or van, which may be difficult to determine in practice. Employers will need to make sure that any reimbursement made towards the cost of electricity relates solely to the charging of their company car or van.

It should be remembered that where the employee uses workplace charging facilities there is no taxable benefit.

It should be noted that HMRC have still not revised their view on reclaiming VAT in respect of business miles driven by an employee who has changed their car at home. Regardless of whether the vehicle is a company car or the employee’s own, the employer cannot reclaim the VAT because the supply of electricity is made to the employee, not the employer.

RECLAIMING INPUT VAT ON THE SALE OF SHARES

The sale of shares is an exempt supply for VAT purposes, which means that input VAT on professional fees in connection with the transaction cannot be claimed. However, a recent tax tribunal decision has determined that, under certain circumstances, the input VAT may be claimed. The case concerned the sale of a subsidiary company in order to provide additional funds to complete the building of a new hotel within a hotel group. The taxpayer successfully argued that the costs had been incurred as part of raising funds for the group’s downstream activities generating taxable supplies.

HMRC may be appealing the decision, but in the meantime, companies in a similar position may seek to make protective claims to recover the input tax on professional fees.

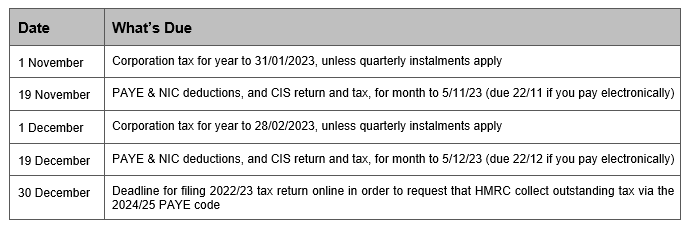

NOVEMBER / DECEMBER 2023

Get in touch

We at PK Group are here to help. You can contact us at welcome@pkgroup.co.uk or via +44 (0)20 8334 9953