With the end of the tax year approaching, it is a good time to start planning your tax affairs before the 5th April arrives.

An obvious tax planning point would be to maximise your ISA allowances for the 2023/24 tax year (currently £20,000 each). You might also want to consider increasing your pension savings before 5 April 2024, as the unused annual pension allowance from 2020/21 lapses after three years. An additional point to consider is whether it is an opportunity to start making or updating your will.

Time to review, or make a will?

At the top of the New Year to do list for many individuals is to make or update their will. Many think this is something to leave until later in life, but it is important to get things in place once property is acquired or when children come along.

In the absence of a will there are statutory rules which dictate how your assets are distributed on death. Those statutory intestacy rules may not be tax efficient, and you might to want to make specific provision in your Will for your unmarried partner or for the guardianship of your children.

People often think that if they die without making a will, their spouse (or civil partner) will automatically inherit everything, but this is not necessarily the case. According to the laws of intestacy in England, for deaths occurring on or after 26 July 2023, the surviving spouse would inherit a statutory legacy of £322,000, all of the personal effects, and half of the remaining estate. The deceased’s surviving children (or their descendants) would split the remaining half of the estate equally. If those descendants are under the age of 18, their inheritance is kept back for them until they turn 18. Note that intestacy rules are different in Scotland, Wales and Northern Ireland.

In addition to income tax, all employees earning more than £12,570 a year pay Class 1 NICs. The main rate of Class 1 NICs will be cut from 12% to 10% from 6 January 2024. This will come into effect from January 2024 and, over a full year, the average worker on £35,400 will receive a NIC reduction of over £450. Workers earning more than £50,270 a year will receive a NIC reduction of £754.

Leaving money in your will to charity

If you leave at least 10% of your estate to charity, the rate of Inheritance tax on the amount chargeable Is reduced from 40% over the nil rate bands to just 36%. This would reduce the amount passing to other beneficiaries and needs to be carefully considered.

Year end inheritance tax planning

Many were expecting an announcement from the Chancellor in the Autumn Statement about cuts to, or the possible abolition of, inheritance tax (IHT). Maybe he is saving that for his Spring Budget, but in the meantime, it may be worth utilising the £3,000 gifts annual exemption for 2023/24 and, if available, the unused amount from 2022/23. Note that £3,000 is the overall exemption for the tax year, not the amount for each done. More generous amounts can be given away by taking advantage of the exemption for regular gifts out of income.

Regular gifts out of your income can save IHT

One tax planning opportunity that many thought the chancellor might restrict was the exemption from inheritance tax for regular gifts out of an individual’s surplus income. Inheritance tax is designed to tax transfers of capital, so if the donor can demonstrate that the gifts are made out of surplus income then the transfers are not taken into consideration for IHT. The exemption applies where there is a regularity to the payments, such as a standing order to pay school fees or pension contributions on behalf of children or grandchildren. HMRC will also require proof that the payments are paid out of post-tax income and do not limit the donor’s normal lifestyle.

Pension contributions on behalf of others

Normally an individual’s payments into a pension scheme are limited to their relevant earnings in a given tax year. This restriction does not apply where the contributions are less than £3,600 gross, allowing parents and grandparents to make payments on behalf of children and grandchildren with limited income. Payments of £2,880 a year would attract a 25% uplift from the government which could grow to a substantial amount by the time the child reaches retirement age (currently age 55, but increasing to 57 in 2028). The parent or grandparent may be able to justify that the payments qualify for the regular gifts out of income exemption from inheritance tax mentioned above if a standing order was set up for no more than £240 a month.

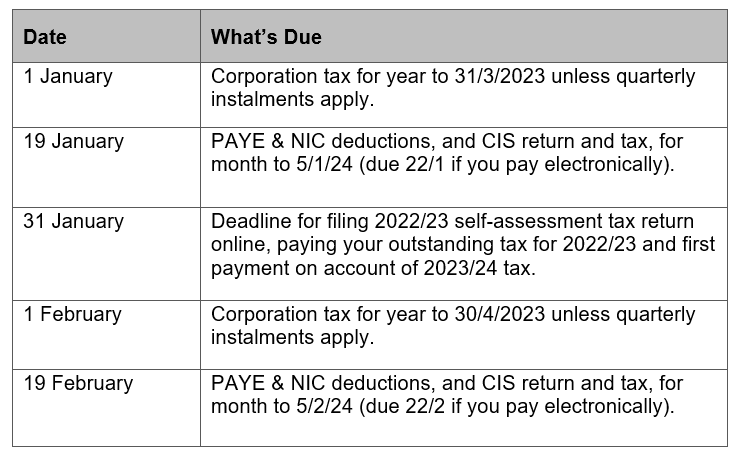

DIARY OF MAIN TAX EVENTS

JANUARY / FEBRUARY 2024

Do you have any further questions? You can contact us at welcome@pkgroup.co.uk or via +44 (0)20 8334 9953