HM Revenue & Customs (HMRC) have introduced a revised penalty regime for the late submission of VAT returns. The new rules apply for VAT accounting periods commencing on or after 1 January 2023 and apply to nil and repayment returns and those for which VAT is paid late. The new penalty system will replace the VAT default surcharge. The way interest is charged is also changing.

Late submission

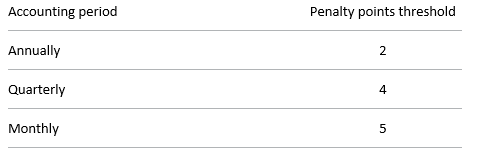

Late submission penalties now work on a points-based system. For each return you submit late, you’ll receive a penalty point until you reach the penalty point threshold. When you reach the threshold, you’ll receive a £200 penalty. You’ll also receive a further £200 penalty for each subsequent late submission while you’re at the threshold. The penalty point threshold is set by your VAT accounting period, and is as follows:

For example, a company submits their VAT Return quarterly. This means their penalty point threshold is 4. They already have 3 penalty points because they submitted 3 previous returns late. They submit their next return late and get a fourth penalty point. Because they’ve reached the penalty point threshold, they receive a £200 penalty. The company submits their next return on time. They stay at threshold of 4 penalty points but do not get a £200 penalty. The company submits their next return late. As they’re still at the penalty point threshold of 4 points, they receive another £200 penalty.

If you’ve not reached the threshold for penalty points for your VAT accounting period, individual points will expire automatically. Your VAT accounting period is when you usually need to send a VAT Return to HMRC, for example quarterly. When penalty points expire depends on the date your return was due. If the deadline for your return was:

• not the last day of a month — a penalty point expires on the last day of the month, 24 months after this

• the last day of a month — a penalty point expires on the last day of the month, 25 months after this

If you’ve reached the penalty points threshold and have the maximum points allowed for your VAT accounting period, you can only remove them by meeting both conditions A and B.

• Condition A: complete a period of compliance, submitting all returns by the deadline. A period of compliance is when you submit all your returns on time.

• Condition B: submit all outstanding returns for the previous 24 months. The 24 months will include the period of compliance.

Late payment interest and penalties

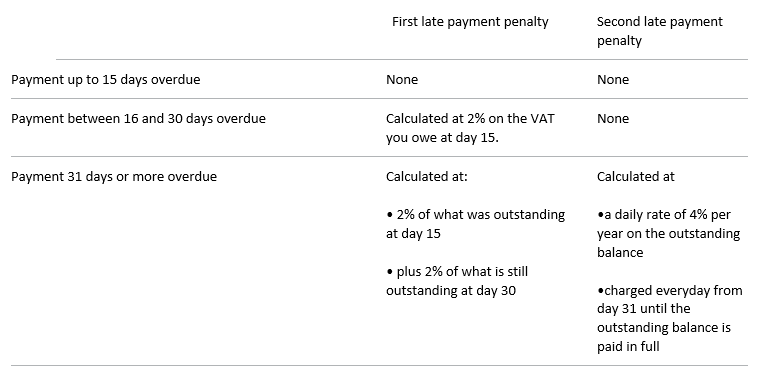

The changes mean that if you pay VAT-related amounts late, you’ll be asked to pay late payment interest on the amount outstanding, from the first day your payment is overdue to the day you pay it in full. If the payment is more than 15 days late, you will also be asked to pay a late payment penalty — the sooner you pay, the smaller the penalty will be. These changes simplify and separate penalties and interest.

Late payment interest is charged from the first day that the payment is overdue until the day it’s paid in full. It’s calculated at the Bank of England base rate plus 2.5%.

You’ll get a first late payment penalty if your payment is 16 or more days overdue. When your payment is 31 or more days overdue, your first late payment penalty increases, and you get a second late payment penalty. Penalties are calculated as follows:

The new rules also cover non-standard VAT accounting periods, changes in your VAT accounting period, taking over a business and VAT groups. We would be happy to talk you through these changes.

For more information, please do not hesitate to contact us via welcome@pkgroup.co.uk or +44 (0)20 8334 9953