With all of the changes to personal pensions in the Spring Budget, maximising the State Pension entitlement should not be overlooked. The full rate of new State Pension increased to £203.85 per week (£10,600 pa) from 6 April 2023; a 10.1% increase over the 2022/23 rate as a result of the “triple lock” being restored.

At least 10 qualifying years are required to get a UK State Pension, with full State Pension entitlement at 35 qualifying years. Individuals should log into their Government Gateway account to check their contribution record as they may be entitled to credit for missing years, for example if they were on maternity leave or a carer. They can also check how many more qualifying years they need for a full State Pension, and if necessary, make national insurance (NI) contributions for missing years.

Normally it is only possible to make voluntary NI contributions for the past 6 tax years, to top up any missing or partial years. The Government announced an extended deadline to allow taxpayers to make NI contribution in respect of missing years going back to April 2006. This opportunity was originally scheduled to end on 5 April 2023 and was then extended to 31 July 2023. The deadline has now been extended to 5 April 2025.

Class 3 voluntary NI contributions made before 5 April 2025 will be at the Class 3 voluntary NI rates for the 2022/23 tax year of £15.85 per week, or £824.20 for each full year.

SUPER-DEDUCTION REPLACED BY “FULL EXPENSING”

In the Spring Budget the Chancellor announced that “full expensing” – 100% relief for new, eligible plant and machinery – would replace the 130% super-deduction from 1 April 2023 for limited companies. This is in addition to the £1 million annual investment allowance (AIA) and will be available for expenditure incurred up to 31 March 2026.

Unlike with AIA, the equipment must be new and must qualify for inclusion in the capital allowances general pool. The legislation specifically excludes motor cars and assets for leasing. The items purchased are not pooled with other equipment, and a separate record needs to be kept of each piece of equipment. That is because there is a clawback charge based on the disposal value of the asset.

Where the company’s year end straddles 31 March 2023, the amount of super-deduction is pro-rated. For example, if the company had a year end of 30 September 2023, and incurred expenditure on a new machine before 31 March 2023, there would be 115% relief for that equipment. A new lorry purchased in May 2023 would only qualify for 100% full expensing.

Where a company buys new equipment that would normally be dealt with in the capital allowances special rate pool, such as the installation of air conditioning or central heating, the 50% first year allowance (FYA) continues to apply until 31 March 2026. The balance of expenditure would then be dealt with in the special rate pool with a 6% writing down allowance per annum on a reducing balance basis. Where the £1 million AIA is available it would be more advantageous to claim AIA at 100%, rather than the 50% FYA.

SHOULD SMALL BUSINESSES STILL USE THE VAT FLAT RATE SCHEME?

The VAT Flat Rate scheme was introduced in 2002 to simplify VAT reporting for small traders, reducing the time taken to calculate VAT and prepare returns compared to normal VAT accounting. The thresholds for using (£150,000 pa) and exiting the scheme (£230,000 pa) have not changed since 2003. With the extension of Making Tax Digital to all VAT registered businesses, those traders are now required to keep digital records and, arguably, the time saving benefits have reduced. The decision as to whether or not traders should use the scheme should now be based on the amount of VAT payable and the risk of making errors.

Rather than recording and reporting input VAT on business expenses, and then deducting that input VAT from the output VAT on goods and services supplied, the trader merely has to report and pay VAT based on the flat rate percentage for that category of business multiplied by the VAT inclusive receipts. The percentages currently range from 4% for businesses retailing food, newspapers, or children’s clothing to 14.5% for IT consultants and labour only builders, unless the “limited cost trader” rules apply. There is also a 1% reduction in the first year of business as an incentive to use the scheme.

As well as making VAT simple to administer many businesses paid less VAT by using the scheme. Some service businesses allegedly exploited the tax savings, resulting in the government introducing the “limited cost trader” 16.5% rate from April 2017.

What is a “Limited Cost Trader”?

A business is classed as a ‘limited cost trader’ and should use the 16.5% flat rate percentage if the cost of goods purchased is less than either:

- 2% of turnover, or

- £1,000 a year (if cost of goods are more than 2%).

“Goods” excludes expenditure on:

- any services – which is anything that isn’t goods,

- food and drink eaten by yourself or your staff,

- vehicle costs including fuel (unless you’re in the transport sector using your own or a leased vehicle),

- rent, internet, phone bills and accountancy fees,

- gifts, promotional items and donations,

- goods you will resell or hire out unless this is your main business activity,

- training and memberships, and

- capital items for example office equipment, laptops, mobile phones and tablets.

Consequently, many traders supplying services such as IT contractors, management consultants and labour-only builders are likely to be categorised as “limited cost traders” and using normal VAT accounting is likely to mean less VAT is payable.

Potential disadvantages of using a Flat Rate Scheme

The flat rate percentages are calculated in a way that takes into account zero-rated and exempt sales. They also contain an allowance for the VAT you spend on your purchases.

So the VAT Flat Rate Scheme might not be right for your business if:

- you buy mostly standard-rated items, as you cannot generally reclaim any input VAT*,

- you regularly receive a VAT repayment under standard VAT accounting, or

- you make a lot of zero-rated or exempt sales.

*Unless the business purchases a capital item where the VAT inclusive price exceeds £2,000.

Please contact us if you are considering whether or not to use the VAT flat rate scheme for your business.

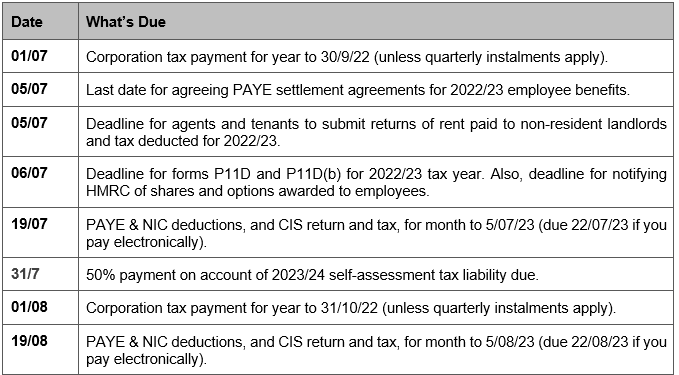

DIARY OF MAIN TAX EVENTS

JULY/ AUGUST 2023